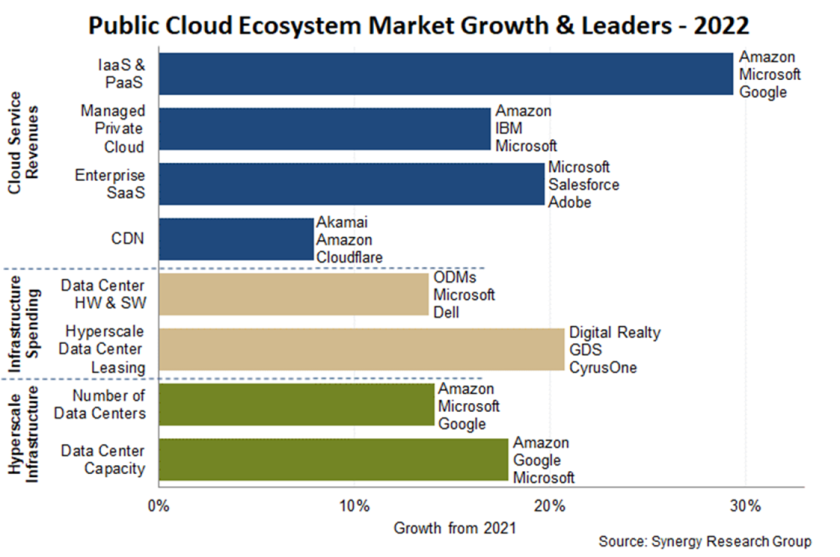

According to new data from Synergy Research Group, the biggest growth was seen in Infrastructure as a Service (IaaS) and Platform as a Service (PaaS). Annual revenue from these services grew by 29% totalling more than $195 billion, despite headwinds from the strong US dollar and problems in the Chinese market.

Across other segments, managed private cloud services, enterprise Software as a Service (SaaS) and content delivery networks (CDN) contributed a further $229 billion in service revenues, having grown roughly 19% from 2021.

Public cloud providers spent $120 billion on building, leasing and equipping their data centre infrastructure, up 13% from the previous year.

Across the entire public cloud ecosystem, there were 15 companies that accounted for 60% of all public cloud-related revenues. The most featured were Microsoft, Amazon, Salesforce and Google. Followed by Adobe, Alibaba, Cisco, Dell, Digital Realty, Huawei, IBM, Inspur, Oracle, SAP and VMware.

Geographically, the US remains a 'centre of gravity', according to Synergy Research Group in 2022, the US accounted for 45% of all cloud service revenues and 53% of hyperscale data centre capacity. The vast majority of leading players in the service and infrastructure space are US companies, followed by Chinese companies who account for 8% of all 2022 cloud service revenues and 16% of hyperscale data centre capacity.

Synergy’s predicts that public cloud ecosystem revenues will double in size in the next four years. During that same period major it expects cloud providers to increase the number of operational hyperscale data centres by 50% and expand the capacity of data centre networks by over 65%.